I’m beginning to see infrastructure P3s not as a product or tool per se but simply as a contractual framework that can allow the public sector to operate outside their normal range of efficiency, risk preference and fiscal constraints. A blank canvas in effect.

Depending on the public sector’s objectives, different “modules” of capability can be added – should be un-bundled, ‘a la carte’ choice, just enough to fulfill the local objectives.

For example, if a large private equity investment and managerial control really deliver significant cost saving and risk transfer compared to public sector, then the classic P3 model makes sense. Works for bigger, complex, high-risk assets with a lot of business-type risk (airports, ports, maybe some tolls roads). But for a lot of simple/low-risk social infrastructure funded by some sort of taxes, the classic module may be overkill.

At the other extreme is the 63-20 or lease type P3 (like NDC or PFG’s “New American Model”) where the contractual framework basically serves as a locus for efficient outsourcing contracts which are outside the normal rules and for off-regulatory/ statutory balance sheet debt. No equity. Very simple, cheap and apparently pretty efficient for social infrastructure with respect to some constraints. But not many – bit of underkill?

The extremes show that the P3 contractual framework is in fact quite flexible. I think the path for P3 innovation – and more widespread adoption – is in developing additional specific modules that can be added to efficiently address specific public sector issues.

As you can tell from this site, InRecap’s focus is on financing modules:

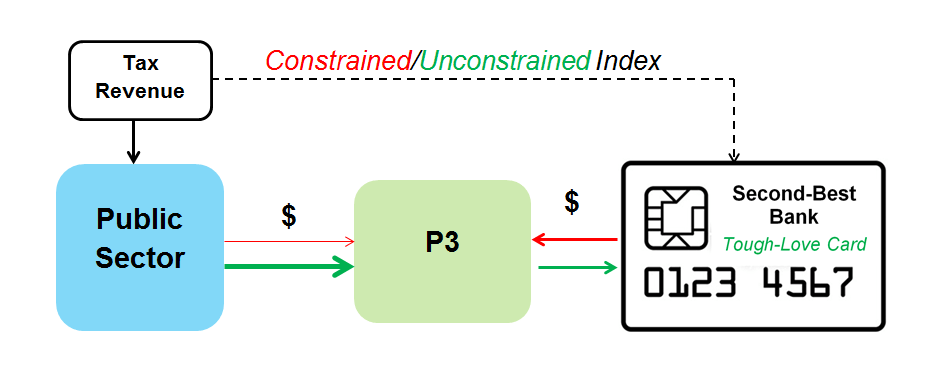

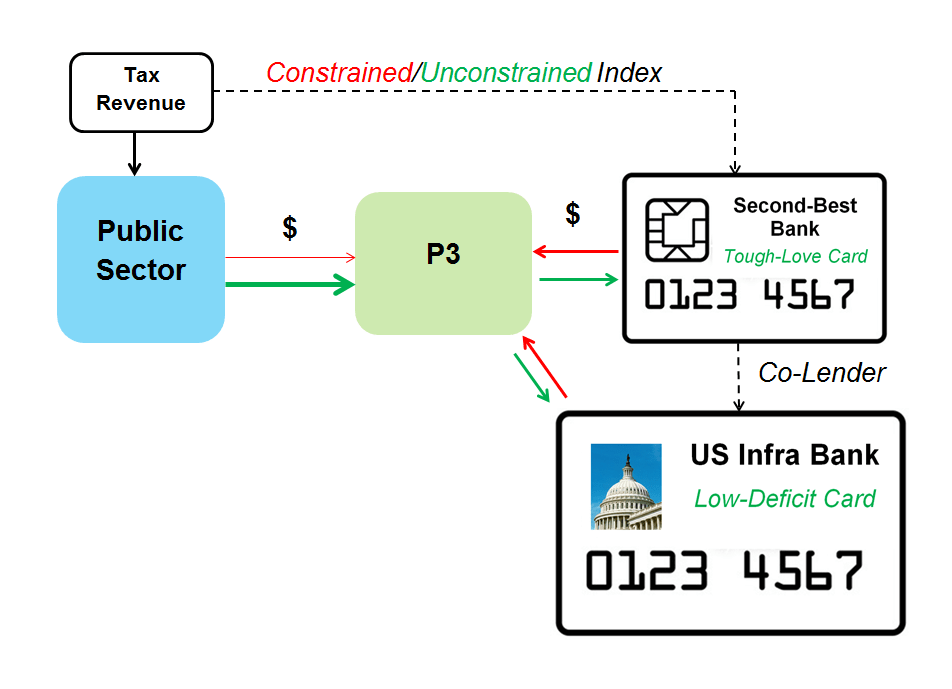

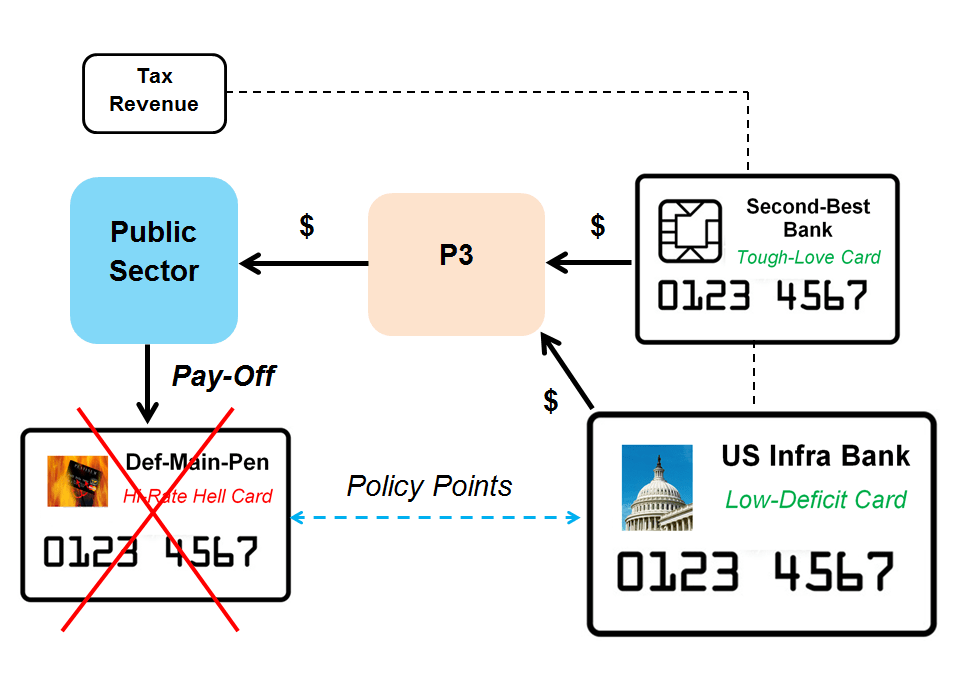

- Built-in rainy day financing: provide some fiscal flexibility during downturns, but disciplined repayment during upturns. Lenders could include project finance banks, debt funds and – ideally – federal/state infrastructure loan programs.

- Social Impact Bond: provide performance-contingent financing for green tech or other aspects of the infrastructure with ESG characteristics. Basic concept is that SIB investors value the ESG aspects more than the local public sector – so transfer makes economic sense

- Dedicated environmental mitigation fund/financing (full credit to Dan Carol of Georgetown University for this idea): concentrate funding/financing resources for environmental permitting/remediation to allow separate optimization (which might be very different than the rest of the project capitalization)

I think the key to module innovation will be involving expertise/investors that are outside the P3 mainstream – the P3 framework really is flexible and expandable, and the public sector faces a huge range of issues – why not keep the scope of possible solutions and inputs as broad as possible?