As noted in a prior post, a private-sector lender would be willing to offer a climate contingent loan for adaptation infrastructure investment if there was a way to hedge the risk that it won’t be fully repaid if extreme conditions don’t develop. The fundamental nature of the hedge would be a parallel investment that paid more if extreme conditions don’t develop.

It’s not exactly hard to imagine entities with economic exposure to extreme climate change that would very much want some insurance for the all the costs they’ll incur in those possibly disastrous conditions. They’d be willing to pay premiums for an insurance contract that didn’t pay anything if extreme climate conditions don’t develop – in which case the premiums are all gain for the writer of this contract.

So, a portfolio of climate insurance contracts (which will have gains if extreme conditions don’t develop) would hedge a portfolio of climate contingent loans (which will have losses in those conditions). And vice-versa if extreme conditions do develop.

Given the pervasive and precisely measurable nature of climate conditions, the huge scale of exposure on the insurance side and the equally huge need for climate adaptation investment, the raw material for these hedged portfolios is definitely out there. What’s needed is a market to put it all together. Also given (or perhaps, to-be-taken) profit opportunities in such a potentially large and complex market, it will almost certainly develop. One far-sighted firm, Adapting Markets, is already designing and assembling the parts for tradeable securities with yields that will reflect long-term climate outcomes.

Markets, however compelling their fundamentals (or even profit potential), do not emerge overnight. It will take time – which is why, for now, federal programs are the only realistic lender of climate contingent loans. That’s because they can (in the scale of the federal balance sheet), they ought to (since climate adaptation is a Public Good) and, not least, because the federal government needs the climate insurance.

Priming the Pump

However, there’s no reason for federal contingent loan programs to be passive about market development, even if they (unlike private-sector lenders) don’t need it to start underwriting loans. The underwriting and creation of a loan portfolio can be done initially in the context of a Public Good – that is, establish the metrics and evaluate the risk outcomes through benefit-cost analyses with an objective of enabling a level of climate adaptation that’s closer to the societal optimum.

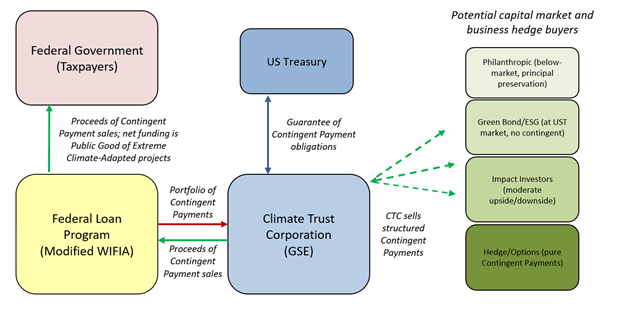

But once a portfolio is created – and many details worked out in the course of doing so – the federal loan programs should put it up for sale. That has two benefits. The first is simply to develop a way for the federal government to manage its risk position in the portfolio. Always good to for a lender to have that tool.

Second, and more importantly, selling a completed loan portfolio is the best way to prime the pump and accelerate market development – because there’s already something to buy.

This process is hardly unprecedented. The Reconstruction Finance Corporation basically started the home mortgage market back in New Deal days. More recently, and more analogously, the Resolution Trust Corporation was established in the 1990s to sell down an existing risk portfolio, federal exposure to foreclosed commercial real estate loans from the S&L crisis. The RTC implemented many financial innovations and successfully developed the CMBS market.

Likewise, a climate contingent loan portfolio can be sold through a separate federally owned GSE – call it the Climate Trust Corporation (CTC) — that will develop marketable securities from the portfolio.

Contingent Loan exposure can be packaged in various forms to meet a broad spectrum of climate-related investor demand, from philanthropic non-market objectives to pure business-related risk hedging. The CTC’s long-term policy objective, consistent with federal infrastructure loan programs, is create a market that eventually will directly offer Climate Contingent Loans to US infrastructure borrowers.

The net proceeds of sales are not intended to, nor likely could, completely reverse the initial FCRA appropriations for Contingent Loan losses, since among other things FCRA uses a risk-free discount rate and market investors will (on average) require a positive risk return. But the net proceeds will establish the current private sector value of extreme climate adaption for infrastructure projects. In effect, the residual FCRA appropriation is the cost of a Public Good that bridges the gap between economic value that can be privatized (by an efficient market) and the BCA-determined optimum value (established by federal review and selection of borrower proposals). As such, the net tax appropriation is more clearly justified as an efficient response to the uncertain possibility of extreme climate change.

Lot of hypotheticals in the details here, of course. But the possibility of future sell-down should be kept in mind while the not-so-hypothetical aspects of a federal contingent loan program are being considered.